Energy of Ukraine

Module 1Lection 2

Advisor to the Minister of Energy of Ukraine (2021-2023), Deputy Minister of Energy of Ukraine (2020-2021) – responsible for policy formation in the oil and gas complex and strategic planning, State Secretary of the Ministry of Energy and Coal Industry of Ukraine, member of the Supervisory Board of SE NPC “Ukrenergo”, Chairman of the Committee on Corporate Governance and Regulation (2018-2019).

In 2014-2016, he headed the department on coal enrichment and quality, functioning of peat mining enterprises and use of coal mine methane at the Ministry of Energy and Coal Industry of Ukraine. He actively participated in the development of the draft law “On the principles of the functioning of the coal market” and the State Standard of Ukraine.

As the Head of the Department for Reforming the Coal Industry of the Ministry of Energy and Coal Industry of Ukraine (2011-2014), he actively participated in the development of draft laws “On the Principles of the Functioning of the Electricity Market”, “On State Support for the Coal Industry”, the Concept on the Transition to the Exchange Form of Coal Sales and other regulatory legal acts.

Has three higher educations: an electrical engineer (Donbas Mining and Metallurgical Institute, 2001), a lawyer (Yaroslav the Wise National Law Academy of Ukraine, 2007), a master’s degree in management and administration (Vadym Hetman Kyiv National Economic University, 2021). Has certificates of completion of training in negotiations, strategic communications in public administration, evaluation and monitoring of policy implementation.

Experience in the energy industry – over 20 years. Worked in companies of various forms of ownership. Has positive experience in enterprise management (including in crisis situations), production management.

Lecture content:

- What is “Ukrainian energy”?

- Resources and networks

- Market and institutional status

- Active links (legal acts, standards, resources)

- Glossary

- Questions for self-testing

1. Introduction. What is “Ukrainian energy”?

Ukrainian energy is a rather complex system that combines several sectors of the economy and is of crucial importance for the life and functioning of our state. It is a very erroneous judgment to say that energy is only the production of electrical energy, its transmission and distribution – in fact, this is not so. Electrical energy must be extracted, produced or obtained from something: from fossil fuels – oil, gas, nuclear resources, or from renewable energy sources – solar, wind, hydro resources, etc.

Extraction of energy resources, their transportation and storage, mechanical engineering and design, construction and operation of generation and networks, functioning of markets and state regulation – all these are components of the energy sector of Ukraine.

2. Resources and networks

Ukraine has almost all the necessary resources to meet its energy needs. Our country also has quite extensive electricity and gas networks – both main and distribution. This adds flexibility and stability to the operation of the Unified State Electric Power System of Ukraine.

Until 2014, we also had a significant reserve of generating capacities. This allowed us to say that Ukraine has significant export potential. But now two of the facilities are in Crimea, and two large power plants – Zuivska and Starobeshivska TPPs – are also in the occupied territories. So the generation losses began 11 years ago. By that time, there were more than enough reserves, as well as resources to ensure generation. Our own coal production fully covered the state’s needs and was even exported. By and large, the same applies to natural gas, which, in my opinion, should be considered primarily not as a resource for electricity production, but as a raw material from which fertilizers, various chemicals, etc. can be produced, and ultimately used for rapid maneuvering and balancing of the energy system.

Distributed generation

To develop distributed generation, we lack an in-depth analysis of how to build it and an understanding of how to manage it. We cannot allow “distributed” generation to replace distributed generation.

Resilience during war

Today we can confidently say that we survived the war and preserved our energy system. Yes, it was very damaged, destroyed, but its synchronous operation in Ukraine was preserved – precisely due to the fact that it is unified, has very developed networks, a sufficient number of substations, options for switching certain consumption zones; the dispatch center worked very efficiently.

Therefore, if we want to build distributed generation, we must preserve the flexibility and maneuverability of our Unified Power System, so as not to get several separate “islands” that will operate independently of each other. This requires both technical and organizational, political, regulatory and legal solutions.

“Green” transition and energy security

The “green” transition that the European Union has set as its goal, which we want to join, is, of course, very good from the point of view of ecology and the future. But we should not forget about our energy security, energy independence and the available technologies that can ensure this “green” transition.

I am deeply convinced that Ukraine as a state, even taking into account the fact that part of its territories are occupied, has significant coal reserves — the deposits are being developed and exploited — and we can fully meet the needs of domestic energy. We also have sufficient reserves of natural gas and even oil. If we develop and use these reserves more effectively, we will be able to provide energy with natural gas of our own production.

Nuclear energy

Ukraine has a developed nuclear energy industry. And we should not forget: even though the Zaporizhzhia NPP is occupied, there are other nuclear power plants that currently provide more than 50% of electricity consumption. We have experienced specialists, the ability to train personnel and extract ore from which nuclear fuel can be produced. So we have all the grounds for the development of nuclear energy.

Large consumers and reserves

If we want to have large industrial producers in Ukraine that consume a sufficient amount of electricity, we must provide them with the production of such an amount of electricity – accordingly, with powerful power plants.

Distributed generation is attractive from the point of view of protection against aggression and maneuvering the system – provided that it is technically combined, and small generation units will not work separately only to meet their own needs, but in an organized manner, under the guidance of a dispatcher, to ensure uninterrupted operation and supportfrequency in the system. But it is difficult for such generators to provide the large capacity needed by large enterprises.

Capacity reservation in the Ukrainian power system is of crucial importance. It is thanks to capacity reserves that we managed to maintain the system and provide electricity to all consumers in Ukraine starting in 2021. A mechanism for paying for capacity reservation is also needed, because if someone builds generation for their own needs, it will be much cheaper for them to pay someone for reservation than to build practically twice as much capacity. This will allow us to be more competitive and less dependent on fluctuations in neighboring markets when merging with the European Union energy market.

Synchronization with ENTSO-E

Our synchronization with the European Union, with ENTSO-E, took place practically on the day of a full-scale invasion. This was a serious challenge for our system. We disconnected from the energy system of Russia and Belarus and worked for some time in an “island” environment. The system coped with the challenge, we showed resilience, and after that synchronization with the European ENTSO-E system took place — thanks to reserves.

Today, technically, our energy system operates synchronously with ENTSO-E, but organizationally we are still far from full integration. Unfortunately, we have already missed the deadline for adopting a law on the integration of our markets — the so-called market coupling, which allows us to unite the markets of Ukraine with the EU markets — by a year. This means full implementation of trade rules, ensuring the fulfillment of contractual obligations, the movement of funds, payment, and access to the intersection. When, when buying volumes in a particular country at joint sessions of the DAM and the IDR, you understand that these volumes are secured, and you do not need to buy the intersection separately — you will receive electricity or sell it.

NEMO: model and integration

We also need to appoint a nominated market operator — NEMO. In the vast majority of countries, a competitive model has been chosen — several such operators compete with each other on price and quality of services, and this has a positive impact on the market. European directives stipulate that each state has the sovereign right to choose a monopoly or competitive model. But if a country chooses a monopoly model, adjacent markets are closed to it from the point of view of the operation of NEMO, which is appointed as a monopoly. If you choose a competitive model, you will be fully integrated. I hope that the bills that provide for a competitive model with a transitional stage to a monopoly model will be adopted.

Integration of the natural gas market and a gas hub

We also expect full integration of the natural gas market. Technically, we have enough intersections, we have one of the largest quantities of underground storage facilities, and there is the potential to establish our own gas hub. Ukraine has the potential to become a European gas hub: significant domestic production and consumption, extensive trunk and distribution systems that combine production, storage facilities, consumers, and export-import opportunities; ports that can accept LNG and have terminals in the future.

To do this, everything must be formalized legislatively and normatively: an exchange form of buying and selling certain volumes of gas in order to have our own indicator (benchmark) of gas prices in Ukraine. The resource must be competitive, the index must be provided with a resource, there is somewhere to store it, and accessibility and simple operation must be guaranteed by law.

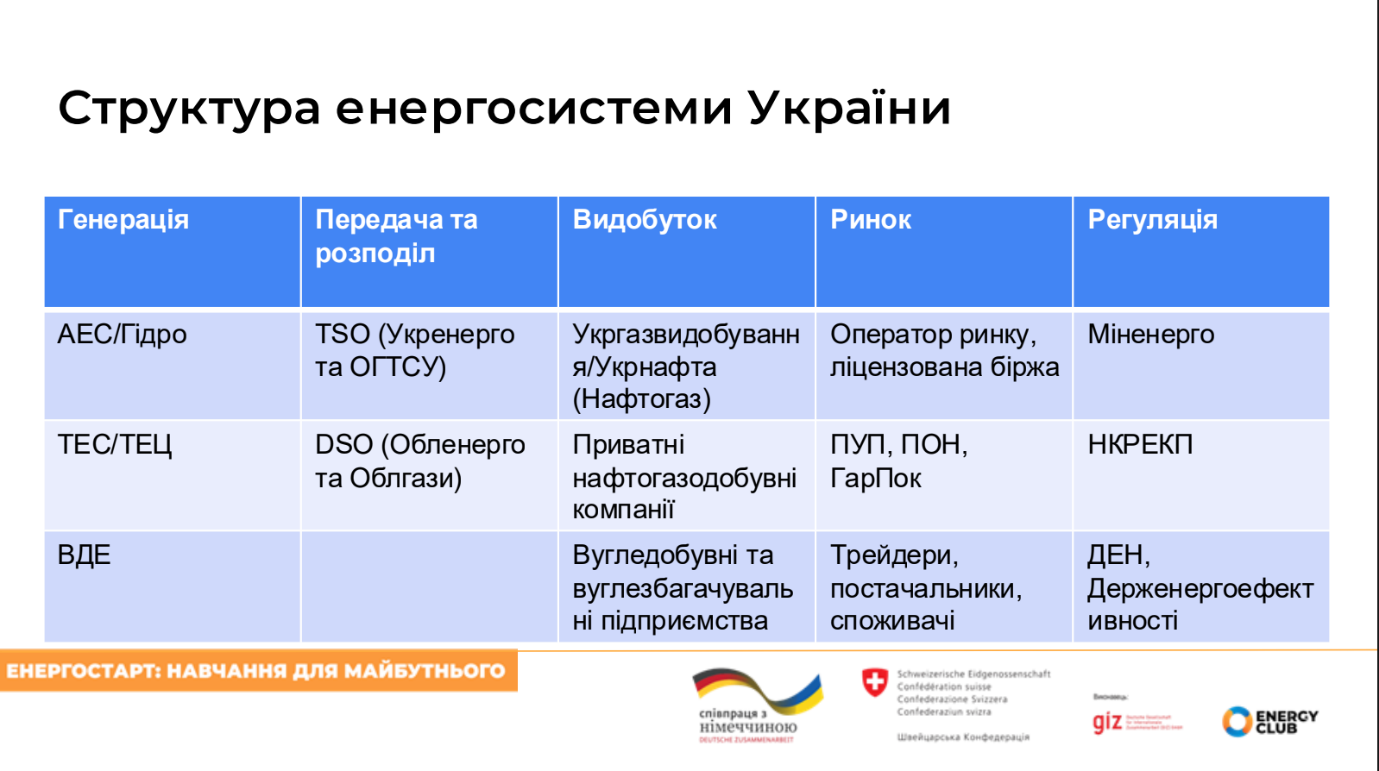

Structure of the Ukrainian energy system

What does our energy system look like in terms of filling with companies, regulation and the formation of a regulatory framework.

We have had changes in the ownership structure of DSOs. Today, most regional gas companies and a significant number of regional energy companies are state-owned, but there are also private companies. In my opinion, after the Victory, we need to return to the fact that DSOs — distribution networks — should be private. This requires appropriate regulation, and from the point of view of European integration, private companies should have the advantage in ownership of networks.

Extraction, processing and added value

Ukraine has great potential for natural gas and oil production – there are enough reserves. We need to attract investments, develop extraction and processing – to obtain more added value. Chemical products and fertilizers have much more added value – this is more beneficial for the economy than burning gas as an energy carrier for electricity generation.

Private companies are developing. For example, DTEK has wells with a depth of over 7,000 meters and is working to increase efficiency and throughput. Moving along this path, we will be able not only to fully provide ourselves with gas, but also to export. As for oil – there is the issue of processing, because, unfortunately, we have difficulties due to enemy attacks.

Coalas an element of energy security

Coal reserves in Ukraine are sufficient for full domestic supply. Enterprises are operating, developments are ongoing. Investments are needed not so much for the construction of new enterprises, but for maintaining energy security and independence. We must have a certain amount of electricity production from coal in our energy mix – provided that environmental requirements are met (modernization or construction of new, more efficient units). We can 100% provide ourselves with this resource – and this is important so as not to depend on other countries.

RES, networks and biomethane

This also applies to RES. We have attractive regions for wind and solar energy. There are issues with electricity supply in certain areas – this is about the development of networks and modernization of equipment for distribution networks and the transmission system operator. The potential for RES in Ukraine is significant.

Given the agricultural potential, there are grounds for producing biomethane — but state support is needed, because we are talking about large capex, the construction of biogas purification chains and product production. It is imperative to ensure integration with the EU market so that our producers can receive additional payments that exist on European markets. Another way: introducing a capacity reserve payment — then biomethane installations will receive a reserve payment plus use biomethane.

3. State of the market and institutions

The market in Ukraine is built almost the same as European markets — we just need to integrate. We have a Market Operator (RDN/VDR), a licensed exchange (futures products), Universal Service Provider (household consumers), Supplier of last resort (guarantee of continuity of consumption). There is a Guaranteed Buyer, which fulfills the requirements of the law and can already sell electricity on the exchange, enter into long-term contracts.

The Ministry of Energy is responsible for the formation of state policy. The National Commission for the Regulation of Energy and Utilities regulates relations in the energy sector and utilities, adopts regulations, codes, and conducts inspections. The State Energy Efficiency Agency and The State Energy Supervision Agency have their own functions and participate in the implementation of the policy (including inspections). We also add the Verkhovna Rada of Ukraine, Antimonopoly Committee and other state structures.

📎 Active links

- Law of Ukraine “On the Electricity Market” No. 2019-VIII (04/13/2017). Official database of the Verkhovna Rada of Ukraine. https://zakon.rada.gov.ua/laws/main/2019-19?utm_source=chatgpt.com#Text

- Transmission System Code (NCRECP, Resolution No. 309 of 14.03.2018) – current version and amendments (including requirements for frequency quality and reserves)

https://zakon.rada.gov.ua/laws/main/v0309874-18?utm_source=chatgpt.com#Text - Law of Ukraine “On the Natural Gas Market” (Vidomosti Verkhovna Rada (VVR), 2015, No. 27, Art. 234) https://zakon.rada.gov.ua/laws/show/329-19#Text

- Regulation of market coupling (CACM): Commission Regulation (EU) 2015/1222 (CACM Guideline): https://eur-lex.europa.eu/eli/reg/2015/1222/oj/eng